Yesterday, at the office, a co-worker in Paris wondered how much time it would take him to get to €1 million, if ever… and proceeded to complain about taxes making it impossible for Europeans to race expats in Dubai, or Singapore, to €1 million capital.

I asked myself, can the European average salary allow enough savings and investments to build €1 million in personal wealth?

In Germany, France, and the UK, a €1 million net worth puts you in the top 5% wealthiest adults.

I started texting my German and English friends, to discuss:

• % of salary paid to social security and taxes

• € spending they require each month to live comfortably

• How they invest their savings, and what capital tax they pay

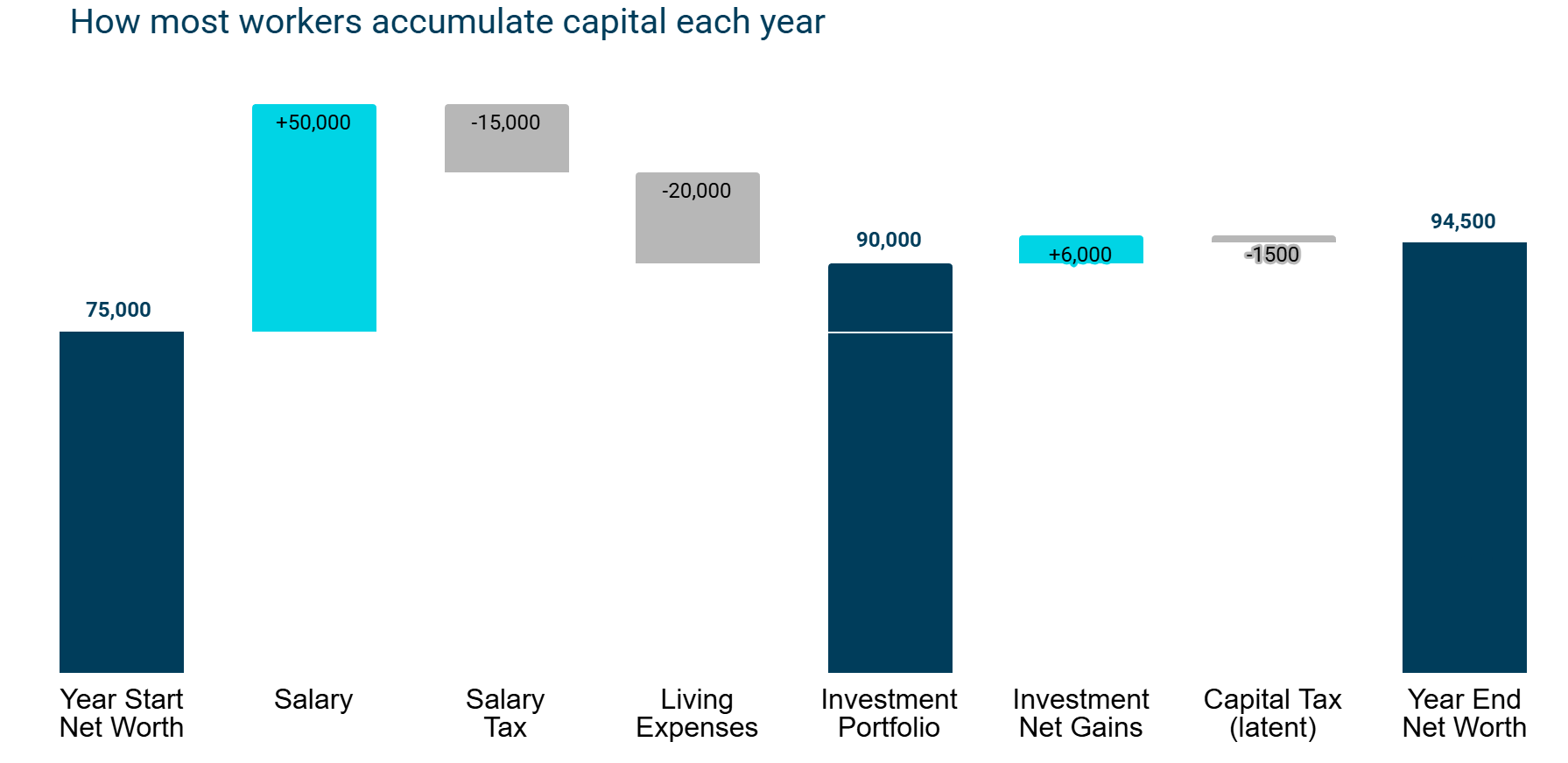

Most salaried workers build wealth by earning their salary, and investing whatever savings are left after paying their taxes and their living expenses. Over the years, the investment gains compound and contribute an ever increasing share of the growth in net worth.

The Take-Home Pay

Say you earn the average wage of the top European economies: Germany, UK, France. Depending on the source, you would earn between 40,000 and 50,000 Euros per year.

The majority of working Western Europeans earn at least 12 times the median salary worldwide.

Matt, Hannah, and Louis are 30-year olds with €65k in savings. They earn a salary equivalent to 50,000 EUR.

Matt

Matt works in the UK with a £43,400 (~€50k) gross salary as of the time of writing. The UK has a high personal allowance: the first £12,570 chunk of his salary is tax-free, and his social contributions are lower. He’s got more cash, but is vulnerable if a health issue hits, and gets a lower state pension.

Take home pay: €3,308 a month

Hannah

Hannah earns €50,000 gross, and pays more labor taxes than Matt to the German state. Germany’s social security system is comprehensive but expensive, taking nearly 21% of her gross pay just for pension, health, unemployment coverage. Germany’s progressive tax scale hits the middle class quickly.

Take home pay: €2,610 a month

Louis

Louis also earns €50,000 gross. His actual income tax is low compared to Hannah, despite being closer to an upper middle class salary in France. But, social contributions are higher (~23% of gross), as healthcare costs and retirement pension are largely covered by the state.

Take home pay: €2,710 a month

| EXPENSES | Matt (UK) | Hannah (DE) | Louis (FR) |

| Gross Salary | €50,000 | €50,000 | €50,000 |

| Social Security | ~€3,500 | ~€10,250 | ~€11,000 |

| Income Tax | ~€6,800 | ~€8,400 | ~€6,500 |

| Take-Home | ~€39,700 | ~€31,350 | ~€32,500 |

| Effective Tax % | 20.6% | 37.3% | 35% |

The Cost of Living and the Savings Rate

Since we’re talking about the middle class, we will focus on tier 2 cities. In Western Europe, a large majority of the population is urban, but on average does not live in the economic capital of the country.

Manchester

Matt witnessed rapid price growth, but Manchester still offers him a much better cost basis than London. Matt’s utilities are high, but his transport costs are manageable as he stays near the tram. His groceries are kept competitive by UK supermarket wars (Aldi v Tesco).

Hamburg

Hannah lives in a wealthy port city, and while cheaper than Munich, it is not cheap. Germany’s energy costs are among the highest in Europe. Hannah’s Warmmiete (rent including heating/water) is a significant chunk of her budget.

Lyon

The 2nd largest French city, Lyon offers a nice quality of life for the price. It retains regional rents lower than Paris. French law often requires employers to reimburse 50% of commuting costs, making Louis’ transport almost negligible.

| EXPENSES | Matt | Hannah | Louis |

| 1 BR rent | 1,150 | 1,100 | 850 |

| Utilities, wifi | 220 | 310 | 215 |

| Groceries | 320 | 350 | 300 |

| Transport | 90 | 49 | 40 |

| Eat out, leisure | 350 | 300 | 250 |

| Total Expenses | 2,130 | 2,109 | 1,655 |

Matt leads the pack. His lower tax burden gives him a massive head start in dry powder to invest in the stock market.

Matt ends the month with €1,180 savings, after cost and taxes.

Hannah has the best worker protections, but high rent and taxes slows down how much money she can invest.

Hannah is left with €506 savings, after cost and taxes.

Louis is a very close second. The lower cost of living in Lyon almost compensates for the higher French taxes.

Louis saves €1,050 after cost and taxes.

Different Capital Tax Rules

In Europe, the taxman collects a slice of your salary; but also a share of the success of your invested savings. The strategies available to Matt, Hannah, and Louis create a massive divide in their final net wealth.

United Kingdom

Capital gains taxes range from 20% to 24%. Except:

ISA: invest up to £20,000 annually for 100% tax-free growth and withdrawals forever.

Workplace pensions: Invest from gross pay to save on Income Tax and 8% National Insurance until age 57.

SIPP: private pension offering an immediate 20% to 45% state top-up on contributions until age 57.

Germany

Capital gains tax is 26.4%. Except:

Sparerpauschbetrag: Realize up to €1,000 in gains per year across all brokerages completely tax-free.

Altersvorsorgedepot (2026): Invest in a SIPP-like account to receive a 20% state subsidy on desposits (up to €600 yearly) plus tax-free growth until retirement.

Speculation Rule: Sell assets like crypto or gold 100% tax-free by holding them for at least 12 months.

France

Capital flat Tax is 31.4%, except for:

PEA/PME equity accounts up to €225k in European equities to eliminate income tax after 5 years, leaving only an 18.2% social charge.

Assurance Vie: accounts allowing withdrawals of up to €4,600 in gains per year income tax-free once the policy is at least 8 years old.

To Each Their Own: Who Wins the €1 Million Race?

We assume all three friends decide to invest mostly in stocks, generating a 7% gross return annually.

Matt decides to max out the employer matching scheme. He then maxes out his ISA, and then invests in a SIPP account, which receives a 20% tax relief (for ‘basic rate’ taxpayers), and 25% of capital gains are Tax-Free; 75% are Taxed as Income.

Hannah decides to use the €1,000 tax-free allowance first, then grabs the 30% state subsidy for retirement, and will invest a tiny portion of her assets into high-risk investments under the 1-year tax-free rule.

Louis keeps 10k in a Livret A.

While the French traditionally prefer Real Estate investments to the stock market, Louis decides to max out his PEA/PME, then invests an Assurance Vie.

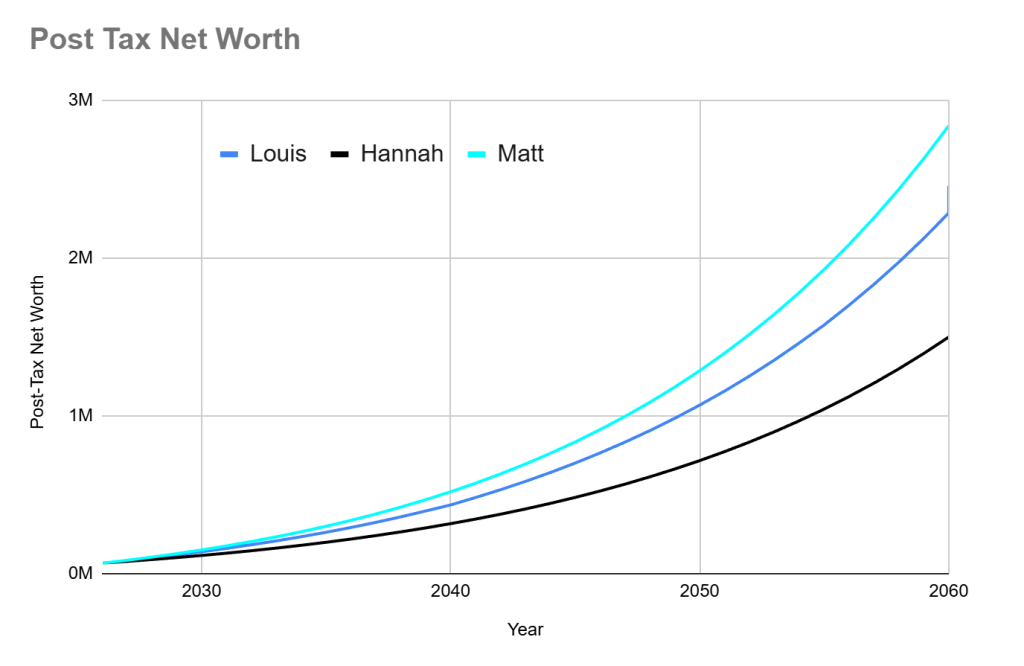

So, who has it better?

Matt, whose financial life is less reliant on state pensions and healthcare coverage, wins the race. Matt reaches €1M equivalent at 52 years old, Louis at 54, and Hannah at 59.

That said, the average salary in Germany is actually higher than France, and Louis’ cheap cost of living in Lyon may not compare to Hamburg. What if all 3 friends had the same costs, and a salary at their respective countries’ average? I checked. Matt situation doesn’t change, but Hannah and Louis fortune reverse. Hannah reach her first million at 55 years old, while Louis has to wait to be 62 years old. That is mainly due the average annual French salary being ~€10k lower than Germany’s.

A word on limitations: while these tax-advantaged pillars provide a massive head start, the Race to €1 Million isn’t run on a level track. Liquidity and Regulatory Risk remain the biggest hurdles: locking capital into a SIPP, PER, or the new German Altersvorsorgedepot means your wealth is technically paper-rich but inaccessible until your late 50s. Also, the very tax benefits that make these accounts attractive, like the UK’s tax-free forever ISA or France’s 8-year Assurance Vie rule, are subject to the whims of future governments, as our Dutch friends experienced this week with their new tax going for vote on unrealized gains. A single budget change can move the finish line just as you’re about to cross it.

Finally, our above models assume consistent market returns and stable exchange rates. Even though we assume 2% inflation, the nature of expenses will evolve; Louis may have to cover for childcare soon. We should keep in mind that a million in 2045 buys significantly less than it does today.

The data shows that a €1 million net worth is achievable on a €50,000 salary, but the timeline depends heavily on your local tax environment. While the UK offers higher immediate savings and tax-free growth through ISAs, France and Germany trade that speed for better social protections, requiring a longer commitment to reach the same goal.

Key Takeaways

Despite identical gross salaries, Matt (UK) saves nearly double what Hannah (Germany) can, in part due to lower initial tax and social drag. Reaching the million-euro mark faster often means having less state-provided security in the short term.

Success requires using specific national accounts like ISA, PEA, or Altersvorsorgedepot to shield gains from capital taxes.

In Europe, the €1 million milestone is a 25-to-35-year marathon. By choosing the right investment mix, your portfolio eventually generates enough lift to sustain itself for the long haul.

Leave a Reply